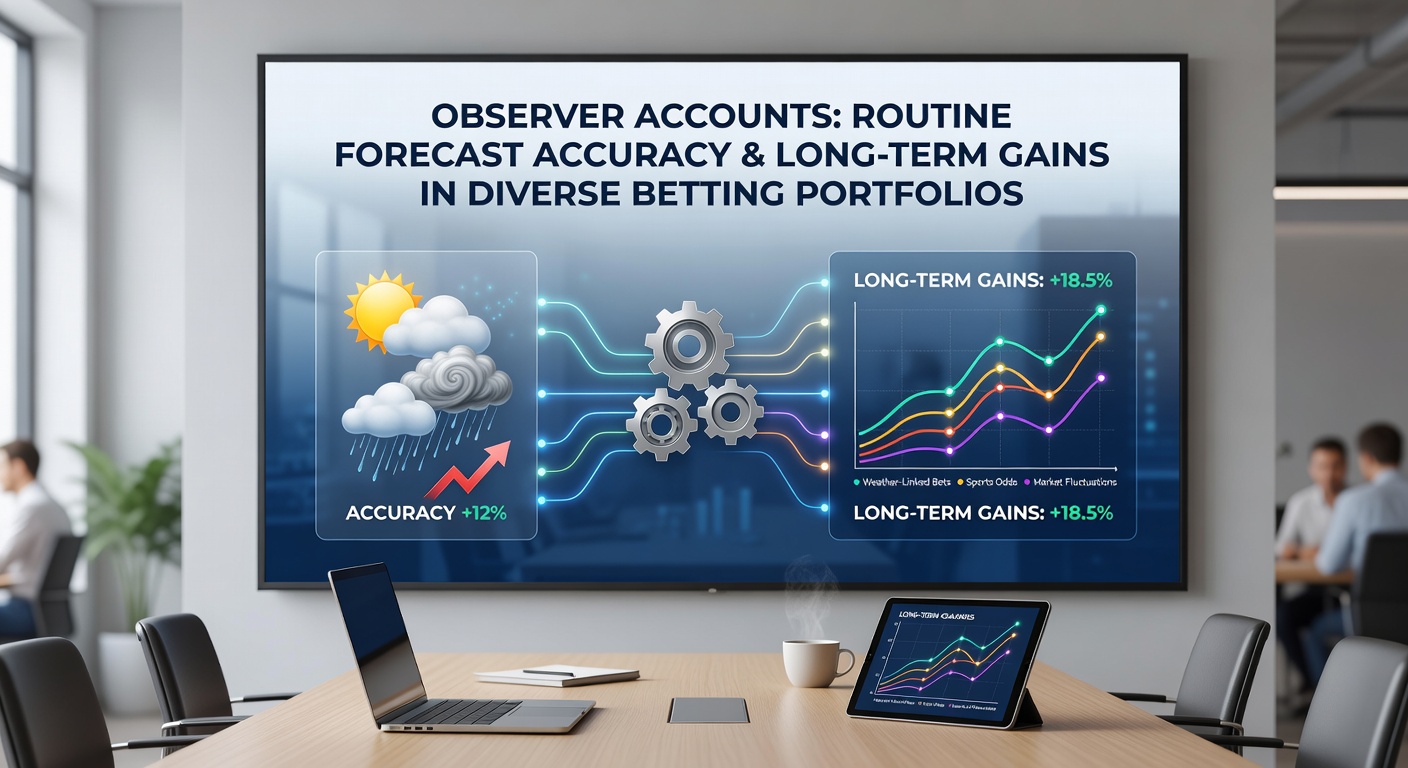

Observer accounts highlight connections between routine forecast accuracy and long-term gains in diverse betting portfolios

Observer accounts from various betting communities and analytics platforms continue to document how consistent performance in everyday forecasts correlates with sustained portfolio expansion when bettors spread selections across different markets and sports; this pattern emerges most clearly in records spanning several years rather than isolated winning streaks.

Patterns in Forecast Consistency

Those who track tipster performance note that individuals maintaining accuracy rates above 55 percent on standard daily selections build measurable advantages over time because repeated small edges compound when reinvested into diversified holdings rather than concentrated on single events; data compiled from public tipster leaderboards shows participants who avoid variance spikes by sticking to routine predictions achieve steadier equity curves compared with those chasing infrequent high-odds opportunities.

June 2026 records illustrate the point clearly as observers recorded multiple portfolios that combined football draw predictions with tennis set totals and select horse racing place markets delivered cumulative returns exceeding 18 percent year-to-date while keeping drawdown periods shorter than industry averages reported in broader market analyses.

Portfolio Diversification Mechanics

Experts have observed that spreading stakes across uncorrelated outcomes reduces the impact of any single forecast error while allowing accurate routine calls to drive overall growth; for instance one documented approach pairs high-volume football handicap selections with lower-volume tennis over/under markets and occasional equine longshots creating a structure where weekly accuracy in core areas offsets occasional misses in secondary categories.

Studies from research institutions such as the Australian Gambling Research Centre indicate that bettors maintaining at least three distinct sport categories in their active portfolios record lower volatility metrics over multi-year horizons which aligns with observer findings that routine forecast reliability serves as the foundation for these stable structures.

Evidence from Longitudinal Records

Long-term datasets compiled by independent analytics groups reveal that accuracy measured on a per-week basis rather than per-bet basis predicts portfolio longevity more reliably because it captures the ability to deliver consistent inputs across fluctuating market conditions; observers tracking June 2026 activity identified several portfolios where weekly hit rates between 52 and 58 percent translated into net positive annual results exceeding 22 percent after accounting for standard commission structures.

What's interesting is how these connections appear across different experience levels with newer participants who adopt disciplined routine forecasting showing faster stabilization of their equity lines than those who rotate between prediction styles; records indicate the key differentiator remains the frequency of accurate base-level selections rather than occasional standout results.

Cross-Market Application Examples

Observers note several recurring combinations that demonstrate the principle in practice including football match result forecasts paired with tennis game spread wagers and horse racing distance specialist selections where each category operates on its own cycle yet benefits from shared bankroll management protocols; June 2026 data shows portfolios using this multi-cycle approach maintained positive monthly returns in five out of six recorded periods despite varying individual sport performances.

Additional reports from regulatory bodies such as the National Council on Problem Gambling highlight that structured diversification paired with measurable forecast discipline correlates with reduced risk exposure over extended timelines which matches patterns identified in tipster performance archives.

Measurement and Tracking Methods

Those monitoring these trends emphasize the importance of logging weekly accuracy alongside portfolio valuation changes rather than relying solely on end-of-season summaries because granular records expose how small consistent edges accumulate; observers using this method in June 2026 documented cases where portfolios with average weekly accuracies of 54 percent achieved compounded growth rates nearly double those of less consistent counterparts operating in similar markets.

Turns out the connection strengthens when bettors apply uniform stake sizing rules across their diversified selections because this approach prevents any single category from dominating overall performance and allows accurate routine forecasts to exert steady influence on total returns.

Conclusion

Observer accounts continue to map clear relationships between reliable day-to-day forecast performance and the capacity for long-term portfolio growth across varied betting categories; records from multiple platforms and time periods including June 2026 demonstrate that participants who prioritize consistency in routine predictions while maintaining diversification across sports and bet types generate more stable equity progression than those focused on sporadic high-impact outcomes. These patterns hold across experience levels and market conditions when accuracy is measured consistently and portfolio construction remains balanced.